Region-by-region economic outlook and latest forecasts for investment returns.

.

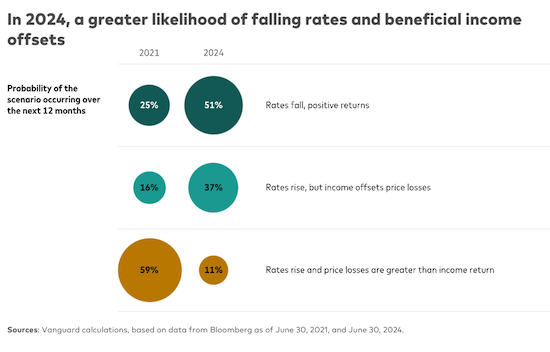

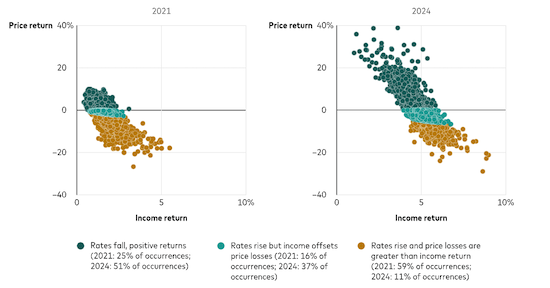

This month, we take a closer look at interest rates and the changed anatomy of bond returns. They’re simple enough dynamics: Interest rates rise, bond prices fall; interest rates fall, bond prices rise. But what happens when you factor in the income that bonds generate? The conditions at the start of an investment matter. And as the charts suggest, initial conditions were far more favourable to bond investors at midyear 2024 than they were at midyear 2021, underscoring Vanguard’s assertion that bonds are back!

An expected boost from bond coupons

Notes: The charts show the 1-year-ahead price and income return projections from the Vanguard Capital Markets Model® for the Bloomberg U.S. Aggregate Bond Index as of June 30, 2021, and June 30, 2024. The forecasts are sorted by positive price returns (interest rates fall) and two scenarios under negative price returns (interest rates rise): income returns from coupons offset price losses, and income returns do not offset price losses, leading to negative total returns.

Sources: Vanguard calculations, based on data from Bloomberg as of June 30, 2021, and June 30, 2024.

Bond yields at midyear 2021 were a paltry 0.25% for the 2-year and 1.45% for the 10-year, compared with midyear 2024 yields of 4.71% for the 2-year and 4.36% for the 10-year. Although it is always difficult to predict short-term outcomes, our simulations as of June 30 of each year showed that the likelihood was much higher in 2024 than in 2021 that interest rates would fall (and bond prices rise). In addition, the likelihood that rates would rise (and bond prices fall) but that income would offset price losses more than doubled in 2024. And as for the prospect of the worst of both worlds—that rates would rise and price losses would be greater than returns from income? It was the most likely outcome in 2021. But in 2024, that scenario was less than 20% as likely to occur as in 2021, our Vanguard Capital Markets Model® (VCMM) projections show.

In 2024, a greater likelihood of falling rates and beneficial income offsets

“Bonds are back, but the prospect of falling rates isn’t the only reason—yield income is higher, too,” said Ian Kresnak, an investment strategy analyst on the VCMM team. “It's the return to sound money, the broad scenario that we laid out in the Vanguard economic and market outlook for 2024. Bonds always play an essential role in a portfolio because they balance out more volatile equities. With coupon payments higher, as they are now, bonds can also withstand some price declines if rates were to rise.”

IMPORTANT: The projections or other information generated by the Vanguard Capital Markets Model regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. Distribution of return outcomes from the VCMM are derived from 10,000 simulations for each modeled asset class. Simulations are as of June 30, 2021, and June 30, 2024. Results from the model may vary with each use and over time. For more information, please see the Notes section.

Vanguard’s outlook for financial markets

We have updated our forecasts for the performance of major asset classes, based on the June 30, 2024, running of the Vanguard Capital Markets Model®. Detailed projections, including annualised return and volatility estimates covering both 10- and 30-year horizons, are available in interactive charts and tables.

Region-by-region outlook

The views below are those of the global economics and markets team of Vanguard Investment Strategy Group as of August 16, 2024.

Australia

Emphasising that it will be “some time yet before inflation is sustainably in the target range,” the Reserve Bank of Australia (RBA) on 6 August left its policy rate unchanged at 4.35%. Vanguard expects the RBA to remain on hold for the rest of the year before beginning a gradual easing cycle amid an anticipated weakening in both inflation and the labour market.

Headline inflation rose to 3.8% in the second quarter on an annual basis from 3.6% in the first quarter, its first increase since the quarter ended December 2022. Given low productivity growth and, as a result, higher unit labour costs, we don’t foresee headline or core inflation falling to the midpoint of the RBA’s 2%–3% target range until 2025.

The economy created more than 58,000 jobs on a seasonally adjusted basis in July, far stronger than expected for a second straight month. The unemployment rate ticked higher, to 4.2% from 4.1% in June, a second straight month of an increase of that magnitude, as the participation rate increased solidly, to a record 67.1%. We expect the unemployment rate to rise to around 4.6% by the end of 2024 as financial conditions tighten in an environment of elevated interest rates.

Demand has weakened in response to the RBA’s restrictive monetary policy, but the economy’s supply side has also been constrained, with lacklustre productivity growth keeping inflationary pressures elevated. GDP rose 1.1% year over year on a seasonally adjusted basis in the first quarter, but was down 1.3% on a per-capita basis for that period.

United States

Recent data suggest that the labour market is softening, and the Federal Reserve appears to be taking notice. The Fed gave a strong signal in July that it was prepared to cut the federal funds rate target by 25 basis points in September. (A basis point is one-hundredth of a percentage point.) We are anticipating an additional second 25-basis-point cut this year and a target range of 3.25%–3.5% at the end of 2025.

The U.S. economy created 114,000 jobs in July, and the unemployment rate rose to 4.3%. The unemployment rate increase is attributable to labour force growth exceeding job growth rather than an increase in job losses.

Broad consumer prices rose in July at the slowest year-over-year pace since early 2021. The Consumer Price Index (CPI) rose by 2.9% compared with July 2023, with shelter price increases accounted for nearly 90% of the monthly increase. The report reaffirms our view that shelter inflation will remain sticky through the rest of the year as supply expands only slowly and demand remains steady.

The Fed’s preferred inflation measure to guide policymaking, the core Personal Consumption Expenditures (PCE) price index, held steady year-over-year in June, rising by 2.6%. We foresee the pace of core PCE rising to 2.9% by year-end because of challenging comparisons with year-earlier data.

The U.S. economy displayed continued resilience in the second quarter, with real GDP growth increasing by an annualised 2.8%, with support from increases in consumer spending, nonresidential fixed investment, and government spending. Through midyear, GDP growth is tracking largely in line with our 2% outlook for the year.

Canada

Softening growth in the labour market and the broader economy amid continued disinflation has led us to lower our year-end 2024 forecast for Canada’s policy interest rate, which the Bank of Canada cut for a second time to 4.5% on July 24. We foresee the equivalent of two to three additional quarter-point rate cuts this year, which would put the overnight rate target in a range of 3.75%-4% at year-end.

The Consumer Price Index report provided further evidence of easing inflation. Headline inflation came in at 2.7% in June on a year-over-year basis, down from a 2.9% rise in May. Core inflation, which excludes volatile food and energy prices, was 2.9% in June on a year-over-year basis, the same level as in May. We foresee core inflation ending 2024 in a range of 2.1%–2.4%.

Household spending helped GDP grow by 0.4% in the first quarter compared with a flat fourth quarter in 2023. We expect below-trend growth for the full year in a range of 1.25%–1.5% amid monetary policy restrictiveness that has been more potent than in the U.S.

The labour market is stagnating, recent data suggest. Canada’s economy shed 2,800 jobs in July, a second straight month of modest job losses, and the unemployment rate held steady at 6.4%. Risks have increased that the unemployment rate could go above our year-end forecast range of 6%–6.5%, as still-restrictive monetary policy could eat into demand and, ultimately, corporate profitability.

Euro area

The euro area’s economy grew by 0.3% in the second quarter compared with the first, according to a flash estimate. An unexpected drag from Germany, where a manufacturing sector rebound remains elusive, was offset by tourism bolstering growth in Spain and France. We foresee full-year GDP growth around 0.8%.

The year-over-year pace of headline inflation increased to 2.6% in July compared with 2.5% in June as there was a reacceleration in services inflation. Core inflation, which excludes volatile food, energy, alcohol, and tobacco prices, remained at 2.9% year over year for a third straight month. We foresee headline inflation falling to around 2.2% by year-end and core inflation falling to around 2.6%, reaching the European Central Bank’s (ECB) target in 2025.

The ECB left its deposit facility rate unchanged at 3.75% in July after a quarter-point rate cut in June. However, we expect further cuts that will put the policy rate at 3.25% at year-end 2024 and 2.25% at year-end 2025.

The unemployment rate rose to 6.5% on a seasonally adjusted basis in June from a record low of 6.4% in May. Although we foresee the unemployment rate ending 2024 around current levels, lower corporate profit margins skew risks to the upside.

United Kingdom

The most recent growth and inflation data suggest the U.K. economy is moving into a better balance. Inflation was softer than expected in July and second-quarter growth was only minimally less than that of the first quarter, when the U.K. exited a brief recession.

The Bank of England (BOE) lowered its policy rate on August 1 by 25 basis points to 5%, the first cut in the current cycle. We foresee one more policy rate cut this year, with the policy rate ending 2024 at 4.75%, and quarterly 25-basis-point cuts in 2025.

GDP increased by 0.6% in the second quarter compared with the first, modestly below 0.7% first-quarter growth. We foresee the economy growing by 1.2% for all of 2024.

The pace of headline inflation increased in July, rising to 2.2% year over year from 2.0% year over year in June, largely owing to energy prices having fallen by less than they did a year earlier.

Core inflation, which excludes volatile food, energy, alcohol, and tobacco prices, slowed to 3.3% year over year in July, from 3.5% in June. We expect core inflation to end 2024 around 2.8% year over year and to hit the BOE’s 2% target by the second half of 2025.

The unemployment rate unexpectedly fell to 4.2% in the April–June period, from 4.4% in the March–May period. We foresee the unemployment rate ending 2024 in a range of 4%–4.5%, but risks skew to the upside given recent signs of labour market softening.

China

Recent broad economic data pointed to a tepid start to the third quarter and a continued imbalance in supply and demand. Fixed asset investment surprised notably to the downside and manufacturing investment slowed. Retail sales provided a bright spot amid increased summer travel and online sales.

GDP grew by 4.7% year over year in the second quarter, reflecting weak domestic demand, sluggish imports, and subdued inflation. We continue to foresee China growing by 5.1% for the full year, though supply and demand that remain out of balance could challenge that growth’s sustainability.

The pace of inflation as measured by consumer prices rose by 0.5% year over year in July, above expectations but well below the PBOC’s 3% inflation target. We expect reflation in 2024 to be mild, with headline inflation of 0.8% and core inflation of just 1.0%.

We expect further monetary policy easing following a surprise rate cut by the People’s Bank of China. The PBOC lowered its new policy benchmark, the seven-day reverse repo rate, from 1.8% to 1.7% on July 22, the first such reduction in the rate since August 2023.

We also expect measures to rescue the housing market, including further relaxation of purchase requirements and cuts to mortgage rates to stimulate demand.

Emerging markets

Progress in the inflation fight is increasingly allowing central banks to focus on economic growth and labour market vitality in their policy-setting considerations. But risks remain that progress in the inflation fight can stall.

Magyar Nemzeti Bank, Hungary’s central bank, cut its policy rate by 25 basis points on July 23, to 6.75%—a 10th consecutive reduction—only to learn that inflation had spiked to a seven-month high in July.

Banco Central do Brasil held its policy Selic rate at 10.5% for a second straight meeting on July 31. It likely found little comfort when headline inflation came in at 4.5% year over year in July, a third straight month of acceleration, and 0.38% month over month.

Banco Central de Chile held its policy rate steady on July 31 at 5.75%. The bank estimated that, if its economic assumptions hold up, the bulk of its 2024 cuts—which currently total 2.5 percentage points—will have already taken place.

Banco de México (Banxico) cut its target for the overnight interbank rate for the second time this year, by 25 basis points, to 10.75%, effective August 9. Vanguard anticipates an additional 50 to 100 basis points of cuts in 2024, to a year-end range of 9.75%–10.25%, levels that would still be restrictive.

Mexico’s GDP growth slowed to 1.1% year over year in the second quarter, down from 1.9% in the first quarter. We expect full-year growth in a range of 1.75%–2.25%, but will be watching for signs of restrictive policy rates weighing on consumption and fixed asset investment.

Notes:

All investing is subject to risk, including the possible loss of the money you invest.

Investments in bonds are subject to interest rate, credit, and inflation risk.

Investments in stocks and bonds issued by non-U.S. companies are subject to risks including country/regional risk and currency risk. These risks are especially high in emerging markets.

IMPORTANT: The projections and other information generated by the Vanguard Capital Markets Model regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. VCMM results will vary with each use and over time.

The VCMM projections are based on a statistical analysis of historical data. Future returns may behave differently from the historical patterns captured in the VCMM. More important, the VCMM may be underestimating extreme negative scenarios unobserved in the historical period on which the model estimation is based.

The Vanguard Capital Markets Model® is a proprietary financial simulation tool developed and maintained by Vanguard’s primary investment research and advice teams. The model forecasts distributions of future returns for a wide array of broad asset classes. Those asset classes include U.S. and international equity markets, several maturities of the U.S. Treasury and corporate fixed income markets, international fixed income markets, U.S. money markets, commodities, and certain alternative investment strategies. The theoretical and empirical foundation for the Vanguard Capital Markets Model is that the returns of various asset classes reflect the compensation investors require for bearing different types of systematic risk (beta). At the core of the model are estimates of the dynamic statistical relationship between risk factors and asset returns, obtained from statistical analysis based on available monthly financial and economic data from as early as 1960. Using a system of estimated equations, the model then applies a Monte Carlo simulation method to project the estimated interrelationships among risk factors and asset classes as well as uncertainty and randomness over time. The model generates a large set of simulated outcomes for each asset class over several time horizons. Forecasts are obtained by computing measures of central tendency in these simulations. Results produced by the tool will vary with each use and over time.

This article contains certain 'forward looking' statements. Forward looking statements, opinions and estimates provided in this article are based on assumptions and contingencies which are subject to change without notice, as are statements about market and industry trends, which are based on interpretations of current market conditions. Forward-looking statements including projections, indications or guidance on future earnings or financial position and estimates are provided as a general guide only and should not be relied upon as an indication or guarantee of future performance. There can be no assurance that actual outcomes will not differ materially from these statements. To the full extent permitted by law, Vanguard Investments Australia Ltd (ABN 72 072 881 086 AFSL 227263) and its directors, officers, employees, advisers, agents and intermediaries disclaim any obligation or undertaking to release any updates or revisions to the information to reflect any change in expectations or assumptions.

General Advice Warning: The information contained on this web site is general in nature and does not take into account your personal situation. You should consider whether the information is appropriate to your needs, and where appropriate, seek professional advice from a financial adviser.

Retirement Planning

Retiring on your own terms is not always easy to achieve, however it is evident that those who plan for retirement are more likely to do so. Results also show that obtaining professional help during the pre-retirement years further improves the probability of attaining your retirement objectives.

The earlier you start implementing a plan the better the outcomes.

During one’s working life there is always an income to make ends meet when raising children, paying off a mortgage, etc.

Retirement planning is about the lifestyle you will have after you stop work and receiving employment income. Planning focuses on issues such as how much superannuation is enough, taking a super pension, claiming the Age Pension, making superannuation contributions while receiving a pension from a super fund, estate planning and looking after your family.

Planning properly is becoming even more important now we are expected to live longer. This greater need means that professional help has never been more important.

At Wybenga Financial we will provide the time and expertise needed to help you implement the best pre-retirement plan possible. Contact us today to discuss how we can work together on: (02) 9300 3000 or .

Building Wealth

Investing your hard earned savings can be a complex task. There are many issues such as levels of risk, market timing, asset classes, and your own goals, objectives and preferences that need to be considered. It can often seem a daunting task. At Wybenga Financial we have the expertise to assist you in taking control of your finances and making sure you are generating the wealth you need both now and in the future.

The first step is to create a plan. At Wybenga Financial we take great care in getting to know our clients and their future goals and objectives. We combine our knowledge of your personal goals together with an analysis of your current situation, to create a detailed, personalised plan that will help you meet your objectives. This plan will become your road map which outlines how we are going to meet your goals, whilst aligning all investment decisions to your specific risk tolerance.

After we have created your personal plan, we move to implementation. This is where we action the immediate changes set out in your plan, and put in place reminders for anything that is to occur in the future. As your professional advisers, we can action many steps on your behalf making the implementation of changes as painless for our clients as possible. We aim to make the process smooth and seamless, providing a holistic service that can be executed with ease.

The final and most important phase of the relationship with Wybenga Financial is the ongoing management of your wealth. This ensures you are sticking to your plan and that your portfolio is aligned to your needs and attitude toward risk. An ongoing relationship ensures that we know when your circumstances change and that these can be recognised and reflected in changes to your investment approach.

While we are reviewing your portfolio from the perspective of your personal goals and situation, we also take into account the wider economic landscape and changes to legislation. We continually review and analyse our preferred investments in a structured and objective way. The benefit to our clients is that we are unemotional. This can be significantly beneficial over the long term.

At Wybenga Financial we can provide the time and expertise that will help you invest intelligently and prudently. Contact us today to discuss how we can work together: (02) 9300 3000 or .

Personal Insurance

Life insurance isn’t just a cost, though it often feels like it. You buy peace-of-mind that should a serious issue effect you then the consequences won’t unduly affect your family. Insurance provides you with the ability to manage the financial and emotional impact of some of the more drastic events, whether personally or in your small business.

Insurance can’t replace a loved one but it can help reduce the financial burden by providing the capital to ensure your family has choices.

Many Australians are underinsured and the consequences can be very serious for families should there be a death or serious injury. A yes to any of the following questions means you may have a need for insurance coverage:

Do you have a mortgage?

Do you have school fees?

Do you have any personal loans?

Do you have any credit card debt?

Do you have dependents?

Would your financial position be affected if you were to suffer from an illness or injury?

Do you want to have enough capital to look after your dependents if you were unable to care for them for an extended period of time or perhaps indefinitely?

We understand that it can be difficult determining the type and level of cover you might need, let alone choosing an insurer. We can assist by helping you determine your needs and recommend an insurer that is right for you.

At Wybenga Financial we know how to protect your wealth and will recommend solutions that best suit your needs. Contact us today to discuss how we can work together: (02) 9300 3000 or .

Superannuation

Superannuation is mandatory but taking an early and active interest in your retirement planning is critical to ensuring your benefits are maximised by the time you retire. Many will have a superannuation scheme through employment but increasing numbers are starting their own Self-Managed Super Fund (SMSF).

For many, simply relying on employer contributions may not be enough to provide the lifestyle you desire at retirement. We can assist in building strategies to ensure your retirement goals are met and your required lifestyle is maintained throughout retirement.

It is always best to start saving and planning for your retirement as early as you can.

At Wybenga Financial we know our job is to help you meet your retirement needs and we have the skills and experience to do this for you. Contact us today to discuss how we can work together: (02) 9300 3000 or .

Self Managed Super Funds

Self-Managed Superannuation Funds (SMSFs) offer a good strategy option for many individuals, families and small business owners to build tax effective wealth and to protect assets over time. SMSFs are becoming popular for those who are ready to take control of their own super investments as they give you ultimate control and flexibility to manage your retirement benefits.

It must be noted though, that you will have increased responsibilities as a trustee of the fund. As a SMSF Trustee you need to keep up to date with all required regulations and keep up with the fast paced financial markets.

Wybenga Financial can work with you to understand your personal financial situation and decide whether a SMSF structure is appropriate for you. We will also make sure your assets are invested in the most effective way to maximise your retirement benefits.

Should you wish to consider establishing a SMSF then we can help with all aspects of the process from establishment to managing your compliance obligations.

Wybenga Financial would welcome the opportunity to discuss how we can help maximise your opportunities to grow your wealth through a Self Managed Superannuation Fund (SMSF). Contact us today to discuss how we can work together: (02) 9300 3000 or .

Estate Planning

Your estate is made up of everything you own. This includes your home, property, furniture, car, personal possessions, business, investments, superannuation and bank accounts.

Having an estate plan is extremely important. Having a will is just the first step in your estate plan. It is critical to consider what outcomes you would like for your estate and to ensure a plan is in place to achieve those outcomes, both including and beyond the terms of your will.

Wybenga Financial would welcome the opportunity to discuss how we can help ensure your estate is organised to ensure your plans are implemented as you wish. Contact us today to discuss how we can work together: (02) 9300 3000 or .

Finance

Loans and loan management are central to overall financial management. Obtaining the the most appropriat loans for your needs is crucial and Wybenga Financial can help you with solutions that meet your short and long term needs.

At Wybenga Financial we work with experienced mortgage brokers that can assist you in obtaining the most appropriate loan for your needs and objectives. Whilst this is an external service, we work closely with the brokers to ensure the process is as easy and smooth as possible.

Contact us today to discuss how we can work together: (02) 9300 3000 or .

Property

We have partnerships with many respected property agents and research firms. This enables us to source suitable properties for individuals, couples and families looking to make an investment into property.

At Wybenga Financial we will assist you implement the most appropriate property investment plan possible. Contact us today to discuss how we can work together: (02) 9300 3000 or .

Strategic Planning

Strategic planning is determining how an investor is going to meet their goals and objectives. It is about helping clients define their goals, gathering information and analysing data to make a plan, then implementing the plan and reviewing the results. It is also reviewing and updating goals and objectives as clients move through different phases of life.

At Wybenga Financial, this is the most critical service we provide. For more information please visit our Building Wealth through Strategic Planning page or contact us to discuss how we can work together: (02) 9300 3000 or .

Financial Videos

Secure File Transfer

Secure File Transfer is a facility that allows the safe and secure exchange of confidential files or documents between you and us.

Email is very convenient in our business world, there is no doubting that. However email messages and attachments can be intercepted by third parties, putting your privacy and identity at risk if used to send confidential files or documents. Secure File Transfer eliminates this risk.

Login to Secure File Transfer, or contact us if you require a username and password.

General Calculators

Please enjoy the links to these free tools supplied by MoneySmart – a great resource for general financial information. Please get in touch if you would like to discuss any questions that you may have as a result of using these calculators.

Tess has been working in Chartered Accounting Firms since 2001 and in this time has had a broad range of experience in superannuation, taxation, business services, and financial strategy.

Since 2016, Tess has turned her attention to Financial Planning, earning a Diploma of Financial Planning in 2015 and leading the newly established financial division of the Wybenga Group as a director of Wybenga Financial.

Tess’s mission is to bring the ethics and integrity of her Chartered Accounting background to the area of wealth management.

As a woman in a male dominated field, Tess is active in promoting gender equality in the industry through various programs and mentoring opportunities.

Using her depth of knowledge and experience in tax and accounting Tess is able to demonstrate a level of competence that is unique in the Financial Planning sector.

2001 – Commenced employment with Wybenga & Partners and part-time accountancy studies

2004 – Graduated Masters of Commerce from the University of New South Wales

2005 – Admitted as an Associate Member of the Institute of Chartered Accountants Australia & New Zealand

2007 – Promoted to Manager at Wybenga & Partners

2012 – Appointed as Associate Director

2015 – Awarded a Diploma of Financial Planning

2016 – Appointed as Director of Wybenga Group Pty Ltd, Wybenga & Parthers Pty Ltd and Wybenga Financial Pty Ltd

Schedule a Meeting with Tess

Adam Roberts

B.Bus, B.Sc, CA, DipFP

Adam has been working in Chartered Accounting Firms since 2005 and in this time has had a broad range of experience in superannuation, taxation, business services, and financial strategy.

Since 2016, Adam has turned his attention to Financial Planning, earning a Diploma of Financial Planning in 2015 and leading the newly established financial division of the Wybenga Group as a director of Wybenga Financial. Adam specialises in Financial Planning, wealth accumulation, portfolion management, tax and investment strategies including structuring investments and superannuation, and insurances.

Adam’s mission is to bring the ethics and integrity of his Chartered Accounting background to the area of wealth management.

Combining traditional accounting and financial services has been a welcome move for Adam, allowing him to operate and advise in the financial sector that has been a long time personal passion.

Using his depth of knowledge and experience in tax and accounting Adam is able to demonstrate a level of competence that is unique in the Financial Planning sector.

2005 – Graduated Bachelor of Science from the University of Western Sydney

2005 – Commenced employment with Wybenga & Partners and part-time accountancy studies

2007 – Graduated Bachelor of Business from the University of Western Sydney

2010 – Admitted as an Associate Member of the Institute of Chartered Accountants Australia & New Zealand

2010 – Promoted to Manager at Wybenga & Partners

2012 – Appointed as Associate Director

2015 – Awarded a Diploma of Financial Planning

2016 – Appointed as Director of Wybenga Group Pty Ltd, Wybenga & Parthers Pty Ltd and Wybenga Financial Pty Ltd

Schedule a Meeting with Adam

Advisory Cadetships

What is an Advisory Cadetship? An Advisory Cadetship enables you to commence your career whilst attaining the necessary university qualifications by studying part-time.

How does it work? Generally, our cadets complete a relevant business or accounting degree at the University of New South Wales, the University of Technology Sydney, Macquarie University, or the University of Western Sydney.

The Firm provides 3-hours paid study leave per week to attend university. This can either be taken at the one time or broken between days depending on the individual’s requirements. In addition, the Firm provides paid study leave for both mid-semester and end-of-year exams.

We take the work life balance very seriously at Wybenga Financial and our cadets are encouraged to have a fulfilling life outside the office. A typical day will have you arriving at the office at around 8.30am with most days concluding at 5.30pm.

What are the benefits of an Advisory Cadetship with Wybenga Financial? Our cadets benefit from the following:

Career path – on completion of their degree our cadets have significant practical experience which will assist them in advancing their careers

Work helps your studies – by working full-time our cadets are able to apply their practical knowledge in the university subjects

Camaraderie with other cadets – the Firm has a number of cadets at various stages of their career

Mentoring – cadets are paired with a senior staff member who oversees their progress and training both at work and with their studies

Communication and feedback – the Firm has an open door policy which enables all cadets to interact with all members of staff including Directors

Culture – the Firm promotes a friendly social culture with a number of functions throughout the year

Modern environment – including ‘socialising’ areas such as pool table and break out area

Training – ongoing support and technical training. We also provide internal and external training on a monthly basis

Remuneration – working full-time provides a market salary and independence with salaries being reviewed every 6-months

What happens when I complete my degree? The completion of your degree is the first step of what we hope to be a long and successful career with us. The next step is the commencement of a Diploma of Financial Planning followed by completing the requirements to become a Certified Financial Planner (CFP).

There are always progression opportunities for the right cadets and we are dedicated to the long term development of our staff.

Who should apply? Current Year 12 students or first/second year University Students who:

want to commence their career in financial advisory;

are due to commence or are currently completing a part-time business or commerce degree at university with an advisory major;

want to gain valuable hands-on experience while completing their qualifications;

are looking for a friendly working environment;

are team players who display initiative;

have a commitment to self-development;

possess excellent personal presentation and communication skills; and

are motivated and mature minded.

How do I apply for an Advisory Cadetship? To apply for a Cadetship position at Wybenga Financial send us your details. Please also include in your covering letter why you wish to do a cadetship, include relevant qualities you possess, main interests / achievements, and any previous employment.

Interested candidates should initially forward a resume/covering letter of no more than 3-pages. Please provide full details of contact information (telephone or e-mail).

What if I have more questions? For further information about our Cadetship program, please send your enquiry to .